AML/CTF Law Changes – Tipping Off Offence Update

By Vicki Guo at 02/04/2025

Your information is securely held, communications are safely encrypted. Our fully encrypted backups occur often and regularly. Flexible and secure user password security.

Fast interfaces, user experience and reporting through the latest database design and web technology. User management tools aide efficient processes

Uncluttered user interfaces, multiple browser tab access, effortless data links. Our user-friendly and easy to learn user interface means no steep learning curve. Logical data entry flow with what you expect where you expect.

You select the modules you use and customise to your needs. You control your reports' content, you tailor your installation to suit your businesses needs

We support the global standards on Risk Management (ISO 31000) and Compliance (ISO 19600) and APRA SSP 220

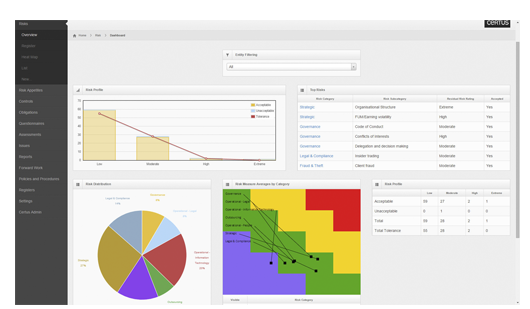

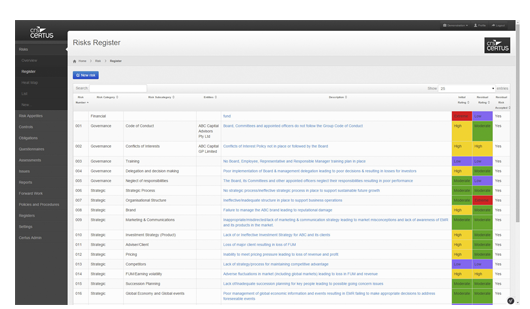

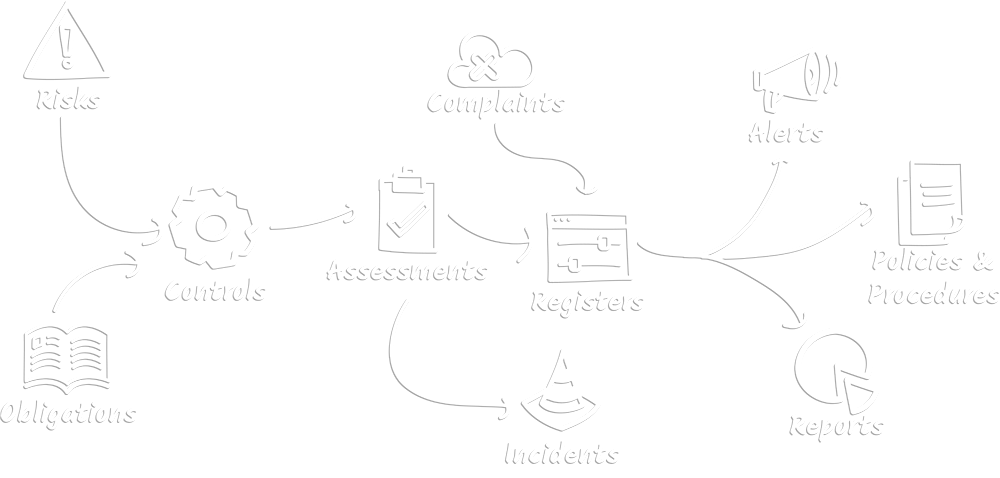

One stop for all of your risk and compliance office needs. View completed and incomplete controls. Retain all your controls and records in the one accessable data base

CRS Certus becomes your record of your risks, risk profile, risk mitigators, obligations, responsible managers and staff, policies and procedures. It holds your proof of control execution. It facilitates recording and managing issues, incidents and complaints. CRS Certus can be interrogated to deliver reports on all data it holds in a format your audience needs.

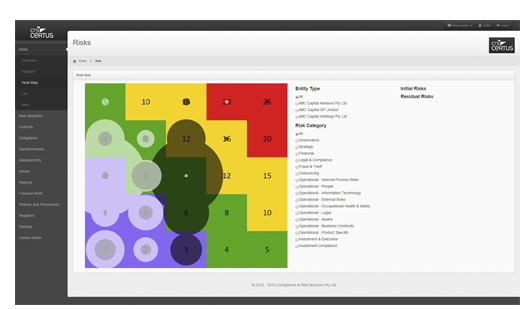

Full risk management system. Customisable risk register. Multiple entity ratings support. Links to mitigating controls and issues register. Risk appetites tied to strategic objectives. Risk tolerance triggers and questionnaire system.

Record obligations. Link to legislative or regulatory sources. Reconcile obligations with business controls

Document business controls. Link to risks and obligations. Assign responsibilities to managers. Automatically generate controls self-assessment questionnaires. Managers alerted when questionnaires are ready, complete within CRS Certus

Controls response assessment navigation. Record testing results. Full audit records of resolution and further action. Directly load adverse responses into Issues Register.

Capture incidents originating from within CRS Certus and reported by your business. Customise incident categories. Workflow management. Assign activities. Capture reportability assessment, related documents and developments.

Customise complaint categories. Seamless flag as incidents, breaches or risk mitigation controls failures.

Breach register with regulator reporting assessments. Personal dealing approvals and register, gifts & benefits, training, conflicts of interest, relatedy party, legal documents, administrative documents, publications, office holder registers amongst others.

Email alerts issued out of the system directed to your defined positions. Customisable email content and triggers. Email service log validates that communications are sent.

Policies and procedures library. Alert users to new content to review within CRS Certus. Capture user confirms of access and understanding of policies and procedures. The library becomes your single point of truth.

Flexible reporting to PDF and XLS(X). Customisable report content, period and presentation, tailored and relevant for the audience. Reports returned immediately. Aides regulatory enquiry, annual audit, demonstrates the control you have over your business

In addition to providing CRS-Certus as a software service, we provide consulting and outsourced management services. These services are available separately from CRS-Certus.

We can help to:

Compliance & Risk Services Pty Ltd has been providing risk and compliance management solutions for businesses for over 10 years.

We have particular experience with financial Australian financial institutions such as Australian Financial Services Licensee, APRA regulated entities, Australian Credit licensees and AUSTRAC reporting entities.

We are experienced risk and compliance management practitioners experienced in developing and operating risk and compliance management systems.

CRS-Certus is developed through our experience as risk and compliance management practitioners.

Our programming team is retained in-house. We believe that the partnership of practitioner and programmer provides a strength that few competitors may match.

Our system uses contemporary database design, programming languages, and hardware. We have implemented a constant backup regime using offsite encrypted storage.

We have provided services to over 200 clients over the globe. We have acted as topic experts under ASIC enforceable undertakings, engaged as experts in litigation and ASX disciplinary reviews.

Key Changes Effective Now:

Businesses and individuals bound by AML/CTF laws must now assess whether disclosing information could prejudice an investigation before sharing it (other than with AUSTRAC).

The updated tipping off offence focuses on potential harm, with penalties remaining severe (up to $39,000 or 2 years’ imprisonment).

Purpose:

Balances intelligence gathering with practicality to enhance crime detection while preventing criminals from being alerted.

Encourages legitimate information sharing within and between businesses to combat money laundering and terrorism financing.

AUSTRAC’s Stance:

Reforms modernize outdated laws ahead of expanding coverage to 100,000+ new businesses (e.g., real estate, accountants) in 2026.

Goal: Strengthen collaboration between industry and law enforcement without compromising investigations.

Next Steps:

Current sectors (banks, casinos, remitters, etc.) must comply immediately.

Additional AML/CTF obligations for newly regulated industries take effect in 2026.

Action Required: Review disclosure protocols to ensure compliance with the harm-based test.

Feel free to drop us a message if you have any questions or requests.

Or give us a call at

P: 03 9663 4456

and post us at

P.O. Box 18009

Collins Street East

Melbourne, VIC 8003

We're located at

Suite 2, Level 47, 80 Collins Street (North Tower)

Melbourne, VIC, 3000